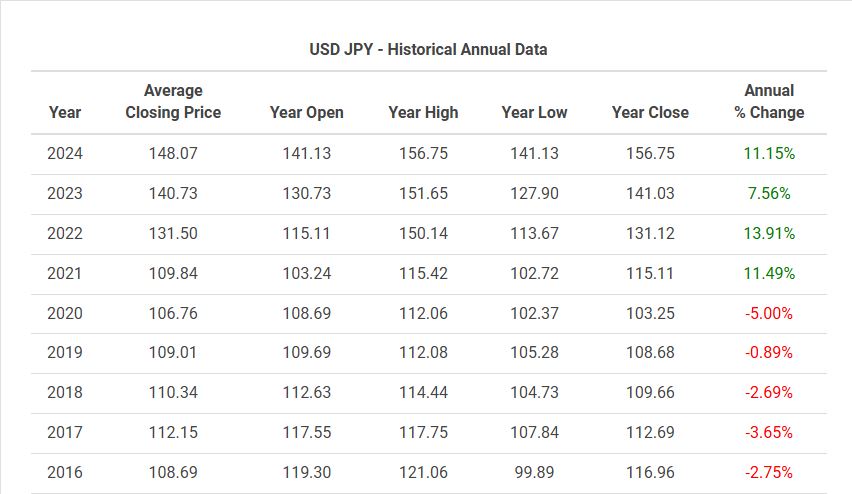

Once considered a symbol of economic stability and strength, the Japanese yen has seen a considerable decrease in value against currencies like the US Dollar and Euro. The yen’s weakness has come under renewed scrutiny following its recent value decline. The currency fell to 160.17 versus the US dollar, the lowest since April 1990.

A country’s currency’s value fluctuates between other currencies by supply and demand regulations. Investors are currently selling the yen due to a wide gap in interest rates between Japan and the United States.

While the US Federal Reserve’s benchmark interest rate is now fixed at 5.25–5.50 percent, the Bank of Japan’s (BOJ) equivalent rate is at 0-0.1 percent.

The devaluation of the Japanese yen is caused by a complex combination of economic policies, global market dynamics, internal obstacles, and political factors, with significant consequences for the country’s economy and inhabitants.

Why the decline?

A series of complex domestic and international economic policies contribute to the present fall of the yen against the US currency. Firstly, the Bank of Japan’s (BOJ) liberal monetary approach, aimed at stimulating GDP and achieving inflation targets, has led to a weaker Yen.

The BOJ’s ultra-loose monetary policy is driving the yen’s devaluation. The BOJ has used near-zero interest rates and asset purchases to boost economic growth and prevent deflation. Although these initiatives attempt to increase domestic demand and inflation, they have made the yen less appealing to global investors seeking bigger profits.

In contrast, the US Federal Reserve has increased interest rates to combat inflation and attract investors seeking higher profits. The disparity in monetary policy has boosted demand for the US Dollar, further weakening the yen.

The second factor is Currency depreciation, which is further exacerbated by structural economic issues, shifting trade balances, high government debt levels, and political uncertainty. The more investors sell the yen, the lower its value becomes, prompting them to continue selling in a self-perpetuating loop.

Thirdly, the difference in interest rates reflects the vastly different inflation situations in the United States and Japan. While Japan has struggled to raise prices and salaries after decades of economic stagnation, the United States has been trying to keep costs low despite vigorous economic development.

Larger interest rates in the United States allow investors to earn significantly larger returns on investments such as government bonds than in Japan.

Fourthly, the yen’s weakness against other major currencies is exacerbated by inflation and monetary policy disparities. Despite the BOJ’s aggressive monetary easing to maintain a stable inflation rate of approximately 2%, Japan’s inflation remains low compared to other economies. This condition lowers the currency’s purchasing power over time.

On the flip side, rising US and European inflation rates have led central banks to tighten monetary policy and raise interest rates. Japan’s high government debt levels also substantially impact the value of the yen. The debt-to-GDP ratio is among the highest in developed nations, raising concerns about fiscal sustainability. This might weaken the currency. Investors may regard the yen as riskier than currencies from countries with stronger fiscal circumstances.

Lastly, Japan’s economic strategy relies heavily on political stability, but in recent years, it has seen an increase in problems—leadership changes in the ruling Liberal Democratic Party, the LDP, constitutional change talks, and controversial policies, including increasing the defense budget, have created instability.

Japan’s political environment has been shaped by its poor relations with neighboring countries, especially China and South Korea. Trade tensions and diplomatic disagreements can damage investor confidence and economic stability, further influencing the market.

When Japan intervenes to keep the yen from rising, the Ministry of Finance produces short-term notes that raise the yen and are later sold to weaken the Japanese currency. These actions have not significantly boosted long-term growth prospects for the economy.

A new phenomenon?

Historically, the yen has been viewed as a safe haven, drawing investors during global economic turmoil. However, Japan’s trade balance has worsened in recent years. Japan’s trade surpluses have dwindled due to rising energy and raw materials imports and slowing export growth. This move lowers demand for the yen in international markets, leading to its devaluation.

While the yen’s recent collapse has been particularly severe, the currency has been falling steadily since early 2021. Over the past three years, the yen has lost over one-third of its value. The currency has returned to its previous levels following the collapse of a massive asset bubble in the early 1990s. The US Dollar has become the ideal safe-haven asset, especially throughout the COVID-19 pandemic and economic recovery periods.

Due to geopolitical tensions evoked by the Ukraine war and Israeli-Palestine conflicts, investors choose USD and other stable assets over the yen. This move lowers demand for the yen, leading to its depreciation.

Inflation dynamics are another important consideration in currency valuation. Japan has seen low inflation and even deflation during the past two decades. While other countries hiked interest rates to combat inflation surged during the COVID-19 epidemic, Japan maintained rock-bottom borrowing costs to shock the economy out of a longstanding stagnation known as “the lost decades.”

Although the BOJ raised the benchmark rate last month for the first time in 17 years, Asia’s second-largest economy remains a worldwide outlier. Structural difficulties, including an aging population and sluggish productivity growth, have also impeded Japan’s economic performance. These challenges limit the country’s potential for strong economic growth.

What can Japan do about it?

Japanese officials have often expressed alarm about the yen’s excessive devaluation and stated they are willing to act if required. Authorities can use two primary levers: purchasing the yen or hiking interest rates.

The rapid increase in the yen’s value sparked conjecture that officials had intervened in the currency markets to stop its drop, the first such intervention since late 2022. Japanese officials have not verified any intervention in the market, and official figures on whether they did so will not be available until late May.

However, the trend looks to be against a significant rise of the yen shortly. Addressing structural economic issues, maintaining political stability, and implementing balanced monetary and fiscal policies are crucial to stabilizing the yen and promoting long-term economic growth.

A weaker yen benefits Japanese exporters’ profits and tourists visiting Japan who see their currencies go further, but it hurts families by raising import costs. Japan’s political concerns and policy uncertainty complicate the economic situation.

The yen could reach ¥85 per dollar if the Bank of Japan normalizes policy and the Federal Reserve eases. According to the bank, the Japanese currency is currently 30% lower than its ‘equilibrium fair value,’ which is estimated to be roughly ¥100 per dollar.

While other factors influence the yen’s valuation, analysts believe it could reach that level if the Bank of Japan completely normalizes policy, which is still holding its benchmark near zero and implementing unconventional measures such as yield curve control.

The prognosis for Bank of Japan policy is currently uncertain, with incumbent Governor Haruhiko Kuroda preparing to hand over the reins of leadership following his final planned policy meeting this week.

According to Tokyo-based Mizuho Securities, the incoming CEO, Kazuo Ueda, is unlikely to modify policies until the third quarter of this year. However, with global inflation on the rise, pressure is increasing for the BOJ to abandon its longstanding policy of loose money.

saptaparna.cbga@gmail.com